An Indian citizen or a foreign citizen of Indian origin who stays abroad for employment/carrying on business or vocation or under circumstances indicating an intention for an uncertain duration of stay abroad is a NON-RESIDENT INDIAN (NRI). (Those who stay abroad on business visit, medical treatment, study or such other purposes which do not indicate an intention to stay there for an indefinite period will not be considered as NRIs).

A Person of Indian Origin means a citizen of any country (other than Bangladesh or Pakistan),if:

1. He/she at any time held an Indian passport; or

2. He/she or either of his/her parents or grand parents was a citizen of India by virtue of Constitution of India or the Citizenship Act,1955 (57 of 1955); or

3. He/she is a spouse of an Indian citizen, or of a person referred to in (a) or (b)

FII means an institution established or incorporated outside India, which proposes to make investments in Indian securities and is registered with SEBI.

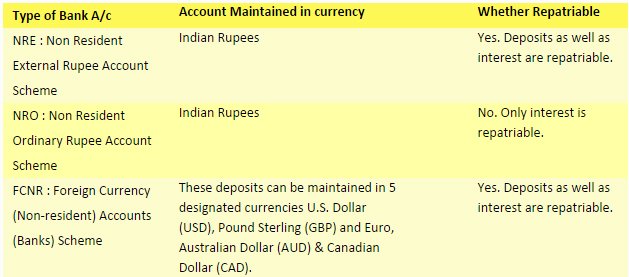

Yes. NRI's can maintain accounts in rupees as well as in foreign currency. Accounts in foreign currencies can, however be maintained in India with authorized dealers only.

Yes. The following summary outlines the various provisions related to investments by Non-Resident Indians ('NRIs'), Persons of Indian Origin ('PIOs') and Foreign Institutional Investors ('FIIs') in the Schemes of the Mutual Fund and is based on the relevant provisions of the Income-tax Act, 1961 ('the Act'), regulations issued under the Foreign Exchange Management Act, 1999 and the Wealth-tax Act, 1957 (collectively called 'the relevant provisions').

NRIs can invest in Mutual funds on a Repatriable/Non-Repatriable basis as per the provisions of Schedule 5 of the Foreign Exchange Management (Transfer or issue of Security by a Person Resident Outside India) Regulations, 2000 ('the Regulations') as explained below.

A Common Application Form duly completed along with cheque or bank drafts should be submitted at Investor Service Centres. The cheque should be made payable at a city where the application is accepted.

Repatriable Basis:

To invest on a repatriable basis, he/she must have an NRE or FCNR Bank Account in India. The Reserve Bank of India (RBI) has granted a general permission to Mutual Funds to offer mutual fund schemes on repatriation basis, subject to the following conditions:

1. The amount representing investment should be received by inward remittance through normal banking channels, or by debit to an NRE / FCNR account of the non-resident investor.

2. The net amount representing the dividend / interest and maturity proceeds of units may be remitted through normal banking channels or credited to NRE / FCNR account of the investor, as desired by him subject to payment of applicable tax.

Non-Repatriable Basis:

The Reserve Bank of India (RBI) has granted a general permission to Mutual Funds to offer mutual fund schemes on non-repatriation basis, subject to the following conditions: Funds for investment should be provided by debit to NRO account of the NRI/ FII investor. Alternatively, funds may be invested by inward remittance or by debit to NRE / FCNR Account.

FIIs may pay for their purchases with funds held in a Foreign Currency account or Non-resident Rupee account maintained in a designated branch of an authorised dealer [Clause 3(1) of the Regulations]. Payments may be made by cheque(s) payable at a city where the application is accepted by Mutual Fund. Applications from FIIs should also be accompanied by appropriate documentation supporting the status of the investor.

Similarly, in case of an application under a Power of Attorney or by an FII, the original Power of Attorney or the relevant resolution/authority to make the application (or a duly notarised certified true copy thereof), along with a certified copy of the Memorandum and Articles of Association and/or bye laws and Certificate of Registration should be submitted to the Mutual Fund. The officials should sign the application under their official designation. The NRIs/PIOs/FIIs shall also furnish other documents needed to process their investments.

An NRI cannot make the investment in foreign currency. He needs to give a Rupee cheque from his NRE, NRO bank account in India. He may also send a Rupee cheque from abroad payable in a bank in India. However, for an NRI to invest, it is mandatory that he maintains a bank account in India.

In order to redeem funds the investor needs to submit the redemption request in original at the nearest Investor Service Centre. All the redemption request forms must contain the Investor's folio number, the amount / unit he would like to redeem and should be duly signed by the Investor or their POA holders. Redemption requests by telephone, telegram, fax or email will not be accepted.

Redemption proceeds will be paid by cheque/transfer to bank account. The cheque will be payable to the first unit holder and will include the bank account number. Alternatively the redemption proceeds will be credited directly to the investors bank account. This facility is available with selected bank as mentioned in our application form. Redemption proceeds/repurchase price and/or dividend or income earned (if any) will be payable in Indian Rupees only. The fund will not be liable for any loss due to exchange fluctuations, while converting the Rupee amount into US Dollar or any other currency.

No.

Repatriation basis: Under the exchange control regulations general permission is granted to authorized dealers to allow repatriation of proceeds of investments made under Repatriable Schemes. The investments shall carry the right of repatriation of capital invested and capital appreciation so long as the investor continues to be a resident outside India, after payment of tax, if any. In the case of an FII, the designated branch of the authorized dealer may allow remittance of net sale/maturity proceeds (after payment of taxes) or credit the amount of sale/ maturity proceeds to the Foreign Currency account or Non-resident Rupee Account of the FII investor maintained in accordance with the approval granted to it by the RBI [Clause 5(i) of the Regulations].

In any other case, where the investment is made out of inward remittance or from funds held in NRE/FCNR account of the investor, the maturity proceeds/repurchase price of units (after payment of taxes) may be credited to NRE/FCNR/NRO Account of the non-resident investor maintained with an authorized dealer in India [Clause 5(ii) of the Regulations].

For transfer to overseas account of the Investor, Mutual Fund will not be responsible and the Investor will have to contact the Authorized dealer for the same.

Non-repatriable basis:

Where the purchase of units is made on a non-repatriable basis, the maturity proceeds / repurchase price of units (after payment of taxes) will not qualify for repatriation out of India and the same may be credited to the NRO account of the non-resident investor [Clause 5(ii) of the Regulations]. However the interest earned on an NRO Account is repatriable.

Similarly, investments in units purchased in Rupees while the investor was resident of India and becomes non-resident subsequently will not qualify for repatriation of repurchase proceeds of units.

The entire income distribution on investment will however qualify for full repatriation. Investors are advised to contact their banks/tax consultants if they desire remittance of the income distribution on units abroad.

No. Investors need to contact their authorised dealers for this service.

As per the taxation laws in force as at the date of updating this document, the tax benefits that are available to the investors investing in the Units of the Scheme(s) are stated herein below.

The tax benefits described in this Document are as available under the present taxation laws and are available subject to relevant conditions. The information given is included only for general purpose and is based on advice received by the AMC regarding the law and practice currently in force in India and the Investors/Investors should be aware that the relevant fiscal rules or their interpretation may change. As is the case with any investment, there can be no guarantee that the tax position or the proposed tax position prevailing at the time of an investment in the Scheme will endure indefinitely. In view of the individual nature of tax consequences, each Investor is advised to consult his/ her own professional tax advisor.

(A) To the Mutual Fund:

The entire income of the Mutual Fund will be exempt from Income Tax in accordance with the provisions of Section 10(23D) of the Income Tax Act, 1961 ("the Act") The Mutual Fund will receive all income without any deduction of tax at source under the provisions of Section 196(iv), of the Act. However, on income distribution, if any, made by the Mutual Fund, the Fund will be liable to pay additional income-tax under Section 115R of the Act, at 12.5% (plus surcharge as applicable from time to time) on the amount of income distributed by the Mutual Fund declared under the schemes on or after April 1, 2003. However, these provisions will not be applicable to any income distributed by an open-ended equity oriented fund (where more than 50 percent of total proceeds of the mutual fund are invested in equity shares of domestic companies as defined in Section 115T of the Act) for a period of one year commencing from April 1, 2003.

(B) Non -Resident Assesses:

The following summary outlines the key tax implications applicable to an NRI / PIO / FII based on the relevant provisions under the Income-tax Act, 1961 ('Act'), Wealth-tax Act, 1957 (collectively called 'the relevant provisions'), subsequent to the amendments enacted by the Finance Act 2003.

i) Income other than Capital Gains As per the provisions of Section 10(35) of the Act, any income received in respect of units of a mutual fund specified under Section 10(23D) of the Act on or after 1.04.2003 is exempt from income tax in the hands of the recipient Investors.

ii) Capital Gains Units of the scheme which are held as capital asset for a period of more than twelve months preceding the date of transfer, will be treated as a long-term capital asset as per the proviso to sub-section (1) to section 112 of Income tax Act. Also, sub-section (7) of section 94 of the Act provides that loss, if any, arising from the sale/transfer of units (including redemption) purchased up to 3 months prior to the record date and sold within 3 months after such date, will not be available for set off to the extent of income distribution (excluding redemptions) on such units claimed as tax exempt by the Investors. Foreign Institutional Investors

Long-term capital gains on sale of Units, would be taxed at the rate of 10% under Section 115AD of the Act. Such gains, would be calculated without indexation of cost of acquisition. Short-term capital gains would be taxed at 30% and without conversion of cost of acquisition and full value of consideration in foreign currency, as the first proviso and second proviso to Section 48 do not apply to Foreign Institutional Investors by virtue of Section 115AD(3) of the Income Tax Act. The said rates would be subject to applicable tax treaty relief. The above tax rates would be increased by applicable surcharge.

No tax would be deductible at source from the capital gains (whether long-term or short-term) arising to an FII on repurchase/redemption of units in view of the provisions of Section 196D(2) of the Act. NRIs/PIOs Long-term and short-term capital gains arising to NRI s /PIO s/ from the transfer of units of the Scheme, will be taxable at the following rates:

A TDS certificate is issued in the name of the investor mentioning the details of the transaction and the tax deducted. The TDS certificate is commonly known as Form16 A.

The digitally signed TDS Certificates (Form 131) are dispatched to the investors once in a quarter.

No, Units cannot be redeemed or allotted on the basis of fax applications. A request that lacks a valid signature cannot be processed due to legal restrictions.

Yes, In a mutual fund the POA has the authority to invest on behalf of the investor and sign documents for initial and additional purchases as well as redemptions. While applying for purchase of units the POA holder needs to submit the original POA or a copy duly notarised should be submitted. The Power of attorney should contain the signature of both the first holder and the POA holder. Only when the POA is registered does the POA holder have the right to transact on behalf of the NRI/FII investor. His signature will be verified for processing any transaction/request.

Yes, It is allowed only for Individuals/HUFs.

Yes, An NRI can be a nominee to an account which is in the name of a resident Indian.

Visit the Reserve Bank of India (RBI) website at www.rbi.org.in.

Switching facility provides investors with an option to transfer the funds amongst different types of schemes or plans. Investors can opt to switch units between Dividend Plan and Growth Plan at NAV based prices. Switching is also allowed into/from other select open-ended schemes currently within the Fund family or schemes that may be launched in the future at NAV based prices.

For applicable NAV, visit AMFI website at: www.amfiindia.com/net-asset-value